In an evolving regulatory landscape, governance and transparency have become key pillars of sustainable growth for NBFCs. The Reserve Bank of India has recently introduced significant amendments concerning lending to related parties, strengthening expectations around credit risk management, financial discipline, and enhanced disclosures. These changes are not merely compliance updates- they signal a sharper regulatory focus on arm’s length transactions, prudent exposure management, and stronger board oversight.

For NBFCs, this is an opportune time to revisit internal lending frameworks, review of policies, related party exposure practices, approvals and disclosure mechanisms to ensure seamless alignment with the revised directions. Early preparedness today can help mitigate regulatory risks tomorrow.

The following amendment Directions were introduced:

- Reserve Bank of India (Non-Banking Financial Companies – Financial Statements: Presentation and Disclosures) Directions, Amendment Directions, 2026

- Reserve Bank of India (Non-Banking Financial Companies – Credit Risk Management) – Amendment Directions, 2026

RPT vs. Lending to Related Parties: Know the difference 🔍

Before diving into the new directions, it is essential to draw a clear line between two concepts that are often conflated: Related Party Transactions (RPTs) and Lending to Related Parties. While RPTs cover the entire spectrum of dealings between an NBFC and its connected entities including purchase of services, asset transfers, and compensation arrangements- lending to related parties is a narrower, credit-specific subset that is now governed by a distinct and more stringent regulatory framework. Understanding this distinction is not just a theory; it determines which approvals you need, what disclosures you must make, and how closely your Board must be involved. Here’s how the two frameworks stack up side-by-side:

| Basis | Related Party Transactions (RPTs) | Lending to Related Parties |

|---|---|---|

| Regulatory Source |

Companies Act 2013 (Section 188) Ind AS 24/ AS 18, SEBI LODR (for listed entities) |

Specific provisions under Reserve Bank of India (Non-Banking Financial Companies- Credit Risk Management)- Amendment Directions, 2026 |

| Scope | Broad scope: RPTs cover any transfer of resources, services, or obligations between the NBFC and a related party (sales, purchases, leases, services, guarantees, compensation, etc.) |

Narrow scope: Funded and Non-funded credit facilities (loans, advances, guarantees, etc.) and investments in debt instruments of related parties. Equity investments excluded. |

| Governance Requirements | Board/ Audit Committee/ Shareholder approval for material RPTs (as per Companies Act and SEBI) | Committee on Lending to Related Parties (Board-level) or any other existing committee (other than Audit Committee) entrusted with sanctioning of loans to related parties or sanctioning authority as per the Credit Policy of the NBFC. |

| Approval Mechanism | Approval based on Materiality thresholds under Companies Act. | Committee on lending to related parties or Board. |

| Materiality Thresholds | Varies based on % of turnover, net worth, or paid-up capital under Section 188. |

|

| Monitoring and Controls | Periodic Disclosure and Review (usually annual) | Quarterly internal audit/review, whistle-blower mechanism, and reporting of deviations to Audit Committee. |

| Disclosure Requirements | Nature of relationship, transaction details, outstanding balances (in financial statements and AGM) |

Enhanced specific disclosures:

|

| Applicability | Applies to all companies (including NBFCs) | Applies to Base, Middle and Upper Layer NBFCs (including HFCs); excludes Type 1 NBFCs and Core Investment Companies. Listed NBFCs must also follow SEBI LODR Regulations. |

| Treatment of Existing Exposures | Generally grandfathered unless renewed. | Existing loans in breach can continue to run down (maturity) but cannot be renewed/enhanced without complying with the new norms. |

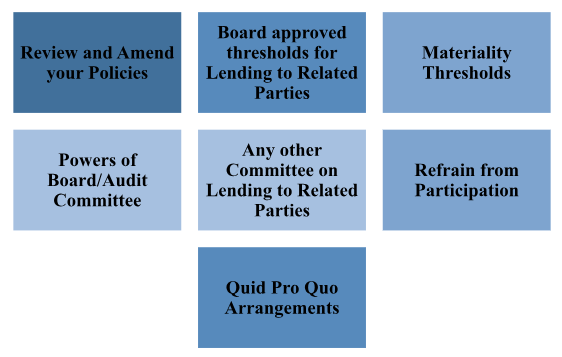

The Golden Rules: General principles of Lending to Related Parties

The Amendment Directions do not simply add more paperwork they fundamentally reshape the governance architecture around related party lending. At the core of these principles is a simple idea: every rupee lent to a connected entity must be justified on the same commercial grounds as a loan to any other borrower. No preferential pricing. No bypassing credit committees. No looking the other way when a director’s relative applies for a facility. The principles below form the non-negotiable bedrock of a compliant and credible lending framework:

- Review and Amend your Policies – Every NBFC should revisit its existing Credit Policy and/or Related Party Transactions Policy to align with the amended RBI directions. The policy should clearly define related parties, approval processes, exposure limits, due diligence standards, monitoring mechanisms, and reporting obligations for lending to related parties

- Board approved thresholds for Lending to Related Parties – The Board is required to approve monetary thresholds beyond which proposals for lending to related parties shall require higher-level scrutiny and sanction by the competent authority / designated committee / Board, as may be applicable under the internal framework.

- Materiality Thresholds – Credit facilities to related parties may be extended by an NBFC in accordance with its Board-approved credit policy. However, all such loans, including personal loans granted to directors or Key Managerial Personnel (KMPs), shall be subject to materiality thresholds which shall not exceed ₹10 crore for Upper Layer and Top Layer NBFCs, ₹5 crore for Middle Layer NBFCs, and ₹1 crore for Base Layer NBFCs. These thresholds shall apply at the individual transaction level. NBFCs may prescribe different thresholds for different categories of loans or borrowers, provided the same remain within the aforesaid regulatory ceilings.

- Powers of Board/Audit Committee – Where an Audit Committee is constituted, it can be entrusted with oversight of lending to related parties crossing prescribed thresholds. In other cases, such powers may rest with the Board. The objective is independent review of fairness, policy compliance, and prudential impact of such exposures.

- Any other Board-level Committee (other than Audit Committee)- Committee on Lending to Related Parties: The Directions permit NBFCs to designate an appropriate committee of the Board for sanction / review of loans to related parties beyond prescribed limits. Such committee should function independently and in line with the Board-approved policy.

- Quid Pro Quo Arrangements – The Directions prohibit sanction of loans or credit facilities to related parties under reciprocal, accommodation-based, or quid pro quo arrangements. Lending decisions must be based strictly on commercial prudence, creditworthiness, and arm’s length considerations.

- Refrain from Participation – Any director or member having an interest in the concerned related party borrower / transaction is required to abstain from participation in discussions, recommendations, deliberations, or voting in relation to such proposal, so as to avoid conflict of interest

What you must Disclose: Financial Statement Requirements

One of the most consequential shifts in the Amendment Directions is the move towards granular, standardised disclosures in financial statements. Previously, related party lending disclosures were often buried in generic notes, making it difficult for stakeholders to assess the true scale and quality of insider credit exposures. That changes now. NBFCs are required to present a detailed, line-by- line breakdown of related party lending activity- covering not just volumes sanctioned and outstanding, but also the stress status of those loans.

Details of exposures to related parties shall be disclosed as per the following table as stated in amended directions:

| (Amount in ₹ crore) | |||

|---|---|---|---|

| Sl. No. | Particulars | Previous Year | Current Year |

| A. Loans to Related Parties | |||

| 1 | Aggregate value of loans sanctioned to related parties during the year | ||

| 2 | Aggregate value of outstanding loans to related parties as on 31st March | ||

| 3 | Aggregate value of outstanding loans to related parties as a proportion of total credit exposure as on 31st March | ||

| 4 | Aggregate value of outstanding loans to related parties which are categorized as: | ||

| (i) Special mention Accounts as on 31st March | |||

| (ii) Non-Performing Assets as on 31st March | |||

| 5 | Amount of provisions held in respect of loans to related parties as on 31st March | ||

| B. Contracts and Arrangements involving Related Parties | |||

| 6 | Aggregate value of contracts and arrangements awarded to related parties during the year | ||

| 7 | Aggregate value of outstanding contracts and arrangements involving related parties as on 31st March | ||

Your Post-Amendment Action Checklist

Regulatory compliance is not a single event- it is an ongoing discipline. The Amendment Directions come into force with immediate implications for policy frameworks, board committees, internal processes, and reporting systems. The checklist below distils the key actions every NBFC needs to complete to achieve full alignment. Assign clear ownership for each item, set realistic timelines, and treat deviations as audit findings that must be escalated. NBFCs should use this as a living document, revisiting it quarterly as the regulatory environment continues to evolve. Tick each box as your team completes it:

| Compliance Required Post Amendments | Tick |

|---|---|

| Review, amend and formally adopt a revised Credit Policy/Related Party Transactions Policy signed with the regulatory requirements introduced under the Amendment Directions. |

|

| Constitute / designate an appropriate Board Committee for review and sanction of loans or credit exposures to related parties exceeding prescribed materiality thresholds. |

|

| Prescribe Board-approved materiality thresholds for lending to related parties within the regulatory ceilings applicable to the relevant NBFC layer. |

|

|

Prescribe and implement prudential limits and sub-limits for:

(a) aggregate exposures / transactions with all related parties; (b) exposures / transactions with each individual related party; (c) exposures / transactions with a group of related parties. |

|

| Identify, maintain, and periodically update a comprehensive register of all related persons and related parties as per the Amendment Directions, in addition to related party lists maintained under the Companies Act, 2013, applicable SEBI regulations, and accounting standards. |

|

| Report credit facilities sanctioned to specified employees and their relatives to the Board on an annual basis, as required. |

|

| Report any deviations from the approved related party lending policy together with reasons, to the Audit Committee or, where no Audit Committee exists, to the Board. |

|

| Implement controls to detect and prevent circumvention structures, including reciprocal lending, quid pro quo arrangements, or indirect connected lending exposures. |

|

| Ensure conflict-of-interest safeguards, including recusal of interested directors / committee members from deliberations and approvals. |

|

| Conduct awareness and sensitisation sessions for relevant business, credit, and compliance teams on applicable materiality thresholds and the internal Credit Policy framework of the Bank. |

|

| Engage internal auditors to undertake periodic independent reviews of related party lending and exposure controls at quarterly intervals or such shorter frequency as considered appropriate. |

|

| Submit periodic management reports to the Board / Audit Committee on related party exposures, threshold breaches, exceptions, and compliance status. |

|

| Review the framework at regular intervals and update policies, thresholds, and controls based on regulatory changes, business profile, and audit observations. |

|

DISCLAIMER: This checklist is provided for internal compliance purpose only. You may print this and use this as a tool to track your organisation’s compliance process under the requirements introduced under the said amended RBI Directions.

The Bottom Line: Compliance is not a Destination- It’s a direction

The RBI’s Amendment Directions on lending to related parties mark a defining moment for the NBFC sector. These directions are not merely a regulatory obligation to be filed away- they are a signal that the era of opaque insider lending is firmly behind us. NBFCs that rise to meet this standard will not only avoid regulatory censure but will emerge as institutions of greater trust, stronger governance, and deeper investor confidence.

The path forward is clear: review your policies, empower your Board, enforce your thresholds, disclose with transparency, and build a culture where every lending decision, regardless of who is on the other side of the table, is made on merit. Because in the eyes of the regulator, and increasingly in the eyes of the market, how you lend to those closest to you says everything about how you run your institution.

The question is no longer whether your NBFC will comply — it is whether you will lead.