The Definitive Guide to Mergers & Acquisitions: Strategy, Valuation, and Execution in a Volatile Global Market

In the current era of rapid technological disruption and geopolitical shifts, Mergers and Acquisitions (M&A) have evolved from mere financial transactions into survival imperatives. For the modern corporation, M&A is the most potent tool for transformation, allowing firms to bypass years of organic R&D and market entry hurdles. However, the path to a successful closing is fraught with regulatory, financial, and cultural landmines. this guide explores the mechanics of M&A, the rigorous phases of the deal lifecycle, the sophisticated mathematics of valuation, and the emerging trends defining the landscape in 2025.

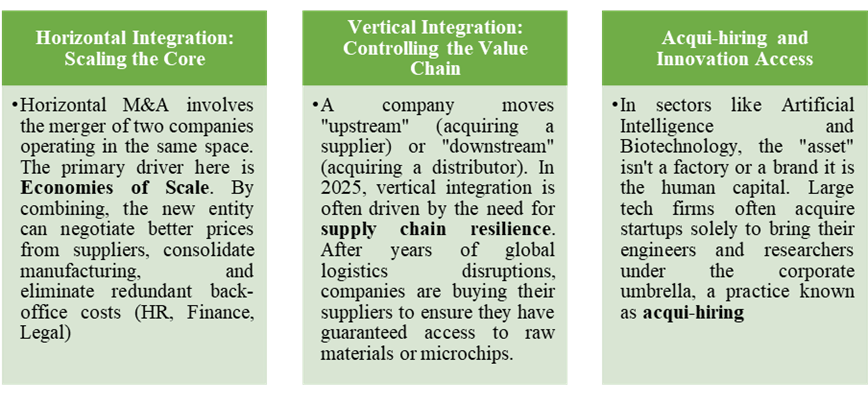

The Strategic Framework

M&A is rarely about buying a company for its current profits; it is about buying a future state that the acquirer cannot achieve alone. Strategically, deals fall into several distinct categories:

The M&A Lifecycle: From Preparation to Integration

A deal is a marathon, not a sprint. The process is generally divided into three major stages: Pre-deal, The Transaction, and Post-deal.

Phase 1: The Pre-Deal Strategy

Before any outreach occurs, the acquirer must perform an internal audit.

- Identify the “Why”: Is the goal to enter the European market? Is it to defensive-buy a competitor?

- The Search Criteria: Establishing “guardrails” for the search, such as revenue size (e.g., $50M–$200M), geography, and EBITDA margins.

- The Teaser and NDA: The initial contact usually involves a “teaser” (an anonymous profile of the target) followed by a Non-Disclosure Agreement before sensitive data shared.

Phase 2: The Due Diligence Deep-Dive

Due diligence is the most critical phase for risk mitigation. It is the process of verifying everything the seller has claimed.

- Financial Due Diligence: analyzing the quality of earnings (QofE). Are the profits sustainable, or were they inflated by one-time events?

- Legal Due Diligence: Checking for “change of control” clauses in existing contracts, pending lawsuits, and intellectual property ownership.

- IT/Cyber Due Diligence: In an era of data breaches, an acquirer must ensure the target’s systems are secure. Buying a company with a hidden back-door vulnerability can result in billions in liabilities.

Phase 3: Post-Merger Integration (PMI)

This is where value is actually created or destroyed. PMI involves:

- System Migration: Moving both companies onto a single ERP or CRM.

- Cultural Alignment: Bridging the gap between different corporate philosophies.

- Synergy Realization: Tracking whether the projected $10M in cost savings are actually being achieved six months after the deal.

The Art and Science of Valuation

Valuation is where finance meets psychology. There is no single “correct” price for a company; there is only a range of values based on different assumptions.

- Discounted Cash Flow (DCF)

The DCF is the “gold standard” of valuation.It posits that a company is worth the sum of all its future cash flows, brought back to today’s value (present value).

The formula for the present value (PV) of a future cash flow is:

PV = CF n

(1 + r) n

Where:

- CFn = Cash flow in year n

- R = The discount rate (usually the Weighted Average Cost of Capital, or WACC)

- N = The number of years into the future

- Comparable Company Analysis (“Comps”)

This is a relative valuation method. If Company A is similar to Company B, and Company B trades at 10x its earnings, then Company A should be valued similarly. Analysts look at ratios like EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization).

- The “Control Premium”

In an acquisition, the buyer almost always pays more than the current market price. This is the Control Premium. It represents the price paid for the right to make decisions, change management, and reap 100% of the synergies.

Deal Structuring: Asset vs. Stock

How a deal is structured has massive tax and liability implications for both parties.

| Feature | Asset Purchase | Stock Purchase |

| What is bought? | Specific equipment, IP, inventory. | The entire legal entity (shares). |

| Liabilities | Buyer picks which liabilities to take. | Buyer inherits all past liabilities. |

| Tax Impact | Buyer can “step up” the basis for depreciation. | Generally more tax-efficient for the seller. |

| Complexity | High (titles for every asset must transfer). | Lower (only shares transfer). |

Why Deals Fail: The “Value Destroyers”

Statistically, more than half of M&A deals fail to create shareholder value. The reasons are consistent across industries:

- The Hubris Premium: The CEO of the acquiring company becomes so obsessed with winning the “bid” that they ignore the financial reality, paying far more than the target can ever return.

- Cultural Incompatibility: “Culture eats strategy for breakfast.” If a rigid, hierarchical company buys a creative, flat-structure startup, the startup’s best employees will quit within 90 days.

- Integration Exhaustion: Management becomes so focused on the deal that they neglect the core business, leading to a drop in performance for both entities.

Modern Trends in 2025

The landscape is currently being reshaped by three primary factors:

- The Rise of “Regulatory Activism” – Antitrust regulators in the US (FTC), EU, and UK have become significantly more aggressive. Deals that would have sailed through a decade ago are now being blocked to prevent “killer acquisitions” where a giant buys a small competitor just to shut them down.

- AI-Powered Due Diligence– In 2025, M&A firms are using Large Language Models (LLMs) to scan thousands of legal documents in seconds. AI can identify “hidden” clauses or risks that a human legal team might take weeks to find, speeding up the deal cycle significantly.

- ESG and Sustainability– Environmental, Social, and Governance (ESG) scores now directly impact valuation. A target with a poor carbon footprint may be “de-valued” because the acquirer knows they will have to spend millions to bring the company up to modern environmental standards.

Conclusion: The Path Forward

Mergers and Acquisitions are the ultimate high-stakes game in business. When done correctly, they create industry titans think of Disney’s acquisition of Marvel, which transformed the film industry. When done poorly, they become cautionary tales like the AOL-Time Warner merger, which destroyed billions in value.

Success in M&A requires a rare combination of financial discipline, legal precision, and emotional intelligence. As we move further into 2025, the winners will be those who use M&A not just to grow bigger, but to grow smarter, more agile, and more resilient.