The RBI has continued its regulatory momentum into February 2026 by releasing a draft amendment to Reserve Bank of India (Non-Banking Financial Companies – Branch Authorisation) Directions, 2025. The amendment aims to simplify branch expansion norms for specific NBFCs while retaining supervisory oversight.

RBI has proposed to remove the need for prior approval or prior intimation for opening new branches by NBFCs. Earlier, several NBFC categories were required to either inform the regulator in advance or obtain specific approval before expanding their branch network. Under the proposed amendment, NBFCs may open branches without such prior permissions, unless specifically restricted under applicable.

This change is particularly significant for gold-loan focused NBFCs, which were earlier required to seek RBI approval once their branch count exceeded 1,000. The amendment also proposes to remove the requirement for Housing Finance Companies, NBFC-ICCs, and deposit-taking NBFCs to obtain prior RBI approval or provide advance intimation for branch expansion, unless specifically restricted under applicable directions. The RBI has made branch expansion faster, simpler, and less paperwork-heavy, helping NBFCs grow their business more smoothly.

What is being proposed?

The draft amendment substitutes the existing branch authorisation frameworks for HFCs, deposit taking NBFCs and NBFC-ICC engaged in lending against gold collateral with a general permission-based approach. Under the amended Directions, NBFCs are permitted to open branches without obtaining prior approval or providing prior intimation to the RBI, unless such opening is specifically restricted under applicable provisions.

This change replaces the earlier approval- and intimation-based regime and applies across NBFC categories, thereby simplifying branch expansion norms and reducing procedural requirements under the Branch Authorisation Directions.

RBI NBFC Branch Expansion: What Has Changed in 2026?

Under the existing framework:

- Deposit-taking NBFCs were required to intimate the RBI before opening branches; unless specifically restricted.

- Housing Finance Companies (HFCs) were required to inform the National Housing Bank prior to branch expansion; and

- NBFC-ICCs engaged in lending against gold collateral who already has more than 1000 branches and wants to expand further were required to obtain prior RBI approval.

The draft amendment deleted these category-specific provisions which were earlier proposed in the directions. As a result, branch expansion for Deposit-taking NBFCs, HFCs and NBFC-ICCs engaged in lending against gold collateral is no longer subject to separate approval or intimation requirements under the Directions.

Branch expansion is now governed by a uniform, principle-based framework, applicable across NBFC categories.

Background and Regulatory Context

In November 2025, the Reserve Bank of India introduced a consolidated framework governing branch authorisation for NBFCs through the RBI (Non-Banking Financial Companies – Branch Authorisation) Directions, 2025. While the framework streamlined and consolidated earlier circulars, it continued to retain prior approval and prior intimation requirements for branch expansion for certain categories of NBFCs, resulting in differentiated compliance obligations.

The February 2026 amendment seeks to rationalise the branch authorisation regime across NBFC categories by replacing the earlier approval- and intimation-based structure with a general permission framework. Under the amended Directions, NBFCs are generally permitted to open branches without obtaining prior regulatory approval or providing prior intimation, unless such branch opening is specifically restricted under applicable provisions.

This amendment reflects a clear shift towards simplifying procedural requirements for branch expansion. While detailed operational guidance, if any, is awaited, the regulatory intent is evident- to reduce advance permissions and move towards governance-led, post-facto supervision, while continuing to expect strong internal controls, effective risk management, and board-level oversight from NBFCs.

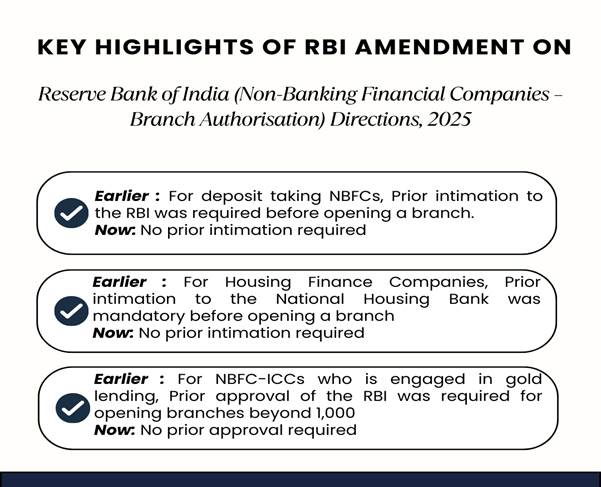

Earlier Rules vs Proposed Change

| TYPE OF NBFC | EARLIER REQUIREMENT | PROPOSED ROLE |

| Deposit-taking NBFCs | Prior intimation before opening branches | No prior intimation required |

| Housing Finance Companies (HFCs) | Prior intimation to NHB before opening branches | No prior intimation required |

| NBFC-ICCs engaged in gold lending | Prior RBI approval for branches beyond 1,000 | No prior approval required |

Key Highlights of the Draft Amendment (February 6, 2026)

1. General Permission to Open Branches

The most significant change introduced by the draft amendment is by allowing HFCs, Deposit taking NBFCs and NBFC-ICC to open branches without prior approval and prior intimation of the RBI. There is no need to stick to hectic process of intimation and approval anymore.

This marks a departure from the earlier regime which mandated intimation or approval-based processes for these NBFCs

2. Deletion of Category-Specific Sub-Regimes

Subsections A2 and A3 of Chapter II- along with paragraphs 7, 8, and 9- have been proposed to be deleted. These provisions earlier imposed intimation and approval obligations on:

- Housing Finance Companies (HFCs), and

- Investment and Credit Companies (NBFC-ICCs), including gold-loan focused entities.

3. Revised Applicability Clause

The amendment also rationalises the applicability provisions by regrouping NBFC categories and clarifying the paragraphs relevant to each class, thereby reducing interpretational ambiguities prevalent under the 2025 Directions.

| From a compliance and operational standpoint, the proposed amendments offer several benefits: |

| Faster geographic expansion for certain NBFCs |

| Reduced procedural formalities and regulatory lag |

| Improved alignment of Reserve Bank of India (Non-Banking Financial Companies – Branch Authorisation) Directions, 2025 |

| Enhanced ease of doing business without compromising prudential oversight |

Way Forward

While the amendment is currently issued as a draft for public comments, it reflects the RBI’s intent to move towards outcome-based regulation rather than procedural supervision. If the drafts gets finalised, the amendment could materially influence branch expansion strategies, compliance structures, and supervisory engagement, reflecting RBI’s broader preference for ex-post oversight over ex-ante approvals.

***A2I Legal continues to monitor regulatory developments closely and advises NBFCs on strategic, compliance-driven implementation of evolving RBI norms***